Family is one of the most important aspects of life, and when it comes to lending and borrowing money among family members, it is important to know the tax implications. Are family loans taxable? The answer may surprise you. In this article we will explore the tax implications of family loans and provide you with the information you need to make sure you are compliant with the tax laws.

What Types of Loans Are Considered Family Loans?

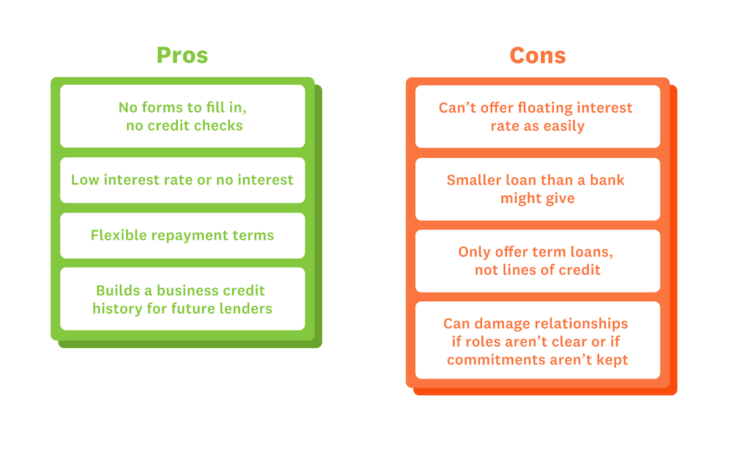

Family loans are a great way to help out a family member without having to go through the hassle of a traditional loan. These loans can come in the form of cash, goods, or services. However, it is important to understand that family loans are taxable and must be reported on your taxes. When it comes to taxes, there are two types of loans that are considered family loans. The first type is an intra-family loan. This is a loan between two family members that does not involve a financial institution. The loan can be for business or personal needs. The second type of loan is an inter-family loan. This is a loan between two family members that involves a financial institution. Both types of loans are taxable and must be reported on your taxes. When it comes to family loans, there are several things to consider. First, you should make sure that the loan is documented and that you have a signed agreement. Second, you should understand the terms of the loan and make sure that the loan is legally enforceable. Finally, you should also be aware of the tax implications associated with the loan. It is important to note that family loans can be a great way to support a family member without having to go

Understanding the Tax Implications of Family Loans

When it comes to family loans, understanding the tax implications is crucial. Generally, loans between family members are not taxable as long as they are properly documented and repayment is expected. However, if the loan is forgiven, the amount forgiven is considered a gift, which is taxable and therefore must be reported. Additionally, if the loan is not adequately documented and the IRS sees it as a gift, it could be subject to gift taxes. It is important to note that the IRS requires a loan to have interest and a repayment schedule. If there is no interest charged and no repayment schedule in place, the loan is viewed as a gift and is subject to taxes. For this reason, it is important to make sure that any family loan is properly documented with an agreement that details the amount of the loan, the interest rate, and the repayment schedule. Additionally, it is important to keep records of repayments to ensure that the loan is not viewed as a gift by the IRS.

How to Structure a Family Loan to Minimize Taxation

When it comes to structuring a family loan to minimize taxation, there are a few key steps that should be taken. First, the loan should be documented in writing. This documentation should include the loan amount, interest rate, term of the loan and repayment schedule. By doing this, you can ensure that the loan is treated as a legitimate loan by the IRS and not as a gift. Secondly, an appropriate interest rate should be set, as the IRS requires that a “reasonable” rate of interest be charged. Lastly, the loan should be reported on both the lender and the borrower’s tax returns. This will ensure that any interest paid is reported as income for the borrower, and as such, it can be deducted from the lender’s taxable income. By taking these steps to structure a family loan, you can minimize the amount of taxation that is due on the loan and ensure that both parties are operating in compliance with the law.

Can You Avoid Paying Taxes on Family Loans?

Taxes can be an unwelcome surprise when it comes to family loans. Fortunately, there are ways to avoid paying taxes on family loans. One way to do this is to ensure that the loan is a true loan and not a gift. A true loan must have a written agreement that outlines the repayment schedule, interest rate, and any other related conditions. Additionally, the loan must have a reasonable interest rate, which is usually the same rate that banks charge on similar loans. The interest rate must also be paid regularly and on time in order to be considered a loan. Finally, any loan amount over $15,000 must be reported to the IRS and is subject to gift tax. By following these guidelines, you can make sure that your family loan is not subject to taxes.

What Happens If You Don’t Pay Taxes on Family Loans?

If you have taken out a loan from family and have not paid taxes on it, you could be facing serious consequences from the IRS. Not paying taxes on a family loan can result in hefty fines, interest, and other penalties. The IRS regards family loans and other gifts as taxable income, and failure to pay taxes on a loan from family can lead to an audit or legal action. It’s important to understand that if you don’t pay taxes on a family loan, you are essentially understating your income. This can lead to serious consequences, so it’s important to be aware of the tax implications of family loans. It’s best to consult with a tax professional to ensure you are properly filing and paying taxes on family loans.